Predicting which technology had the strongest competitive advantages and would ultimately revolutionize any given status quo is an easy task when looking back into the past. Surely anyone could have predicted that touchscreen smartphones with full operating systems would eventually surpass phones with physical keyboards (e.g. Blackberry), that crowdsourced encyclopedia (Wikipedia) would displace expert-curated encyclopedias (Encarta), or that streaming music would replace mp3 downloads (iTunes) [1]. Or would it have not been that easy to predict the future?

With the advent of traditional institutions wanting to ride the blockchain train, a similar dilemma as when the internet was first created has arisen: Should they use private blockchains or public blockchains to protect their data and carry out their business? Which one is the ‘strong’ technology that will outpace both its traditional (centralized) and blockchain counterparts? We will develop a framework for trying to understand and predict (this time into the future) what is the ‘best’ choice.

What makes a technology ‘strong’?

We previously delved into blockchain’s (or ‘DLT’) main benefits, challenges and risks. We also discussed its role in the current state of affairs, and how it can revolutionize every major industry [2]. Yet we haven’t considered the apparent rivalry between the two main types of blockchains: private and public.

To approach this subject, let us present the main differences and similarities between the two:

- Access & Identity. The characteristic that best defines each type of blockchain is the capacity of determining governance protocols and the users access. In a public blockchain, joining the network has no restrictions, so access to the sharer ledger is available to everyone. Private (or permissioned) blockchains have single authorities (usually an organization) that can determine who can join the network and grant specific access and functionalities to each node. They manage this by stripping the anonymity property that characterizes public chains and including identity management solutions.

- Authority. We can understand both types of blockchain as part of a decentralized range; public blockchains are more decentralized, while private ones enjoy the benefit of DLT technology but with a marked authority, arguably making them at best partially decentralized. This characteristic is based on the access and participation any specific individual has in the network. While public blockchains allow anyone to join, private ones need a centralized party to determine user access rights and functionalities.

- Data Handling/Ownership. When combining various categories, a spectrum of data ownership can be found. Public and private networks relate to the degree to which one can write and add to the chain, while open and closed ones relate to who is able to read the data. The easiest case is the known open public blockchains, with available-to-all read and write properties. On the other end of the spectrum, closed private chains don’t even allow for permissionless reading rights [3].

- Transaction speed. Transactions in public blockchains can bottle-neck the network depending on the consensus mechanism used and scaling layers implemented, given that the number of transactions can be exponential to the amount of users. This is not the case for private networks, where only a few have the ability to request modifications of the ledger, thus usually making them faster.

- Consensus. This is one of the most interesting features to analyze. While in original public networks various consensus mechanisms were developed accounting for game-theory based incentive structures, private ones decide beforehand who can join consensus, while most nodes won’t participate in the process.

- Transaction Cost. Similarly to the consensus mechanisms in place for public blockchains, incentive rewards must be paid out to those maintaining the infrastructure of the network (i.e miners/validators). Added to the fact that public blockchains have their own governance coin used to participate in the network (and can appreciate in value), transaction costs end up being very volatile, and even extremely expensive in relation to private chains. Private chains don’t have native coins or incentive structures, thus ensuring constant rates across transactions.

- Immutability. While public networks leverage cryptographic security for full immutability, the fact that smaller, private ones have centralized authorities arranging for permission opens an argument for partial immutability. Under private chains, owners have the authority to decide under which circumstances a verified transaction can be reversed, weighing the benefits and consequences of it (undermined confidence in the system) [4].

- Security. The security pyramid (physical, network, user, application and data) becomes highly relevant within the context of the operating model. Whether it is public, private, or hybrid, the network choice has a direct impact on each level.

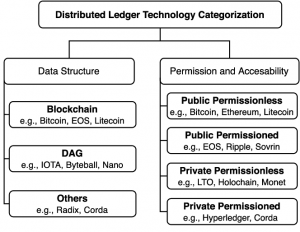

Table I: Categories of distributed ledger technologies [5]

Private & public blockchains: adversaries or associates?

There is a common misconception that public and private blockchains are adversaries, but this could not be further from the truth. How can they be competitors if they are intrinsically different and serve specific needs?

In fact, even public blockchain platforms (like Ethereum) can be used to build private, permissioned scenarios. It would be up to the institutions’ architecture and designer teams, because public networks don’t have private built-in tools, but it is possible. This way, an organization could leverage the security benefits of public blockchains, while keeping a tight grip on information management and security [5].

Additionally, there is one more factor that is rarely taken into account when discussing public/private blockchains, and that is the fact that public blockchains are constantly ‘in the dirt’, and need to work everyday, while private blockchains are synthetically developed in secret rooms, and never tested in the ‘real world’.

Conclusion and the SCALABLE palette

Whether you’d like to leverage the benefits of public, private, hybrid blockchain, or even if you don’t know what’s best for you, at Scalable Solutions we have the knowledge and experience to assist you in every step of the process. We strive for perfection and to provide integral solutions, so even though we understand the benefits of private networks (and are technically equipped to service them), we always recommend running a project in at least one public network.

References

[1] Dixon, Chris. “Strong and Weak Technologies.” Cdixonorg RSS, 18 Jan. 2019, cdixon.org/2019/01/08/strong-and-weak-technologies.

[2] “The Decentralization of Finance (DeFi).” Scalable Solutions, 16 Oct. 2020, scalablesolutions.io/news/the-decentralization-of-finance-defi/.

[3] Winiarsky, Andrzej. “Co-Chains: Bridging Public and Private Chains as a Way to INTEROPERABILITY?” Hacker Noon, 23 Apr. 2020, hackernoon.com/co-chains-bridging-public-and-private-chains-as-a-way-to-interoperability-1y3332kg.

[4] It is true that under public networks the reversal of transactions is possible, but these special occasions are either accepted by the entire community or by some, resulting in hard or soft ‘forks,’ instead of being a single centralized authority deciding. Stay with us, as we will soon discuss forks in greater detail.

[5] Fan, C., Ghaemi, S., Khazaei, H., & Musilek, P. (2020). Performance Evaluation of Blockchain Systems: A Systematic Survey. IEEE Access, 8, 126927-126950.

[6] Massessi, Demiro. “Public Vs Private Blockchain In A Nutshell.” Medium, Coinmonks, 15 Oct. 2020, medium.com/coinmonks/public-vs-private-blockchain-in-a-nutshell-c9fe284fa39f.

General Sources

Anwar, Hasib. “Enterprise Blockchain: The Industrial Transformation.” 101 Blockchains, 14 Nov. 2019, 101blockchains.com/enterprise-blockchain.

Anwar, Hasib. “Public Vs Private Blockchain: How Do They Differ?” 101 Blockchains, 17 Mar. 2020, 101blockchains.com/public-vs-private-blockchain.

Daruwalla, Benazeer, and Charles Carrington. “The Blockchain Is Only as Strong as Its Weakest Link.” Security Intelligence, 23 Apr. 2018, securityintelligence.com/the-blockchain-is-only-as-strong-as-its-weakest-link/.

Peled, Eran. “Private vs Public Blockchain.” Orbs, 26 Feb. 2020, www.orbs.com/private-vs-public-blockchain/.